My kids saw me writing a blog post today that contained a historical chart of S&P 500 returns and asked a few questions about it. I never pass up the opportunity to provide mini economic or financial lectures, so we discussed how stock returns have gone up over time despite disruptive and catastrophic world events, such as the Great Depression, WWII, and the Great Financial Crisis. They seemed to get the concept, then asked if it was time to check their stocks.

I have previously mentioned my lower-middle-class upbringing. My parents worked hard, and we always had enough, but they often struggled financially. There were lots of fights about money, and a pervasive air of uncertainty hung in the air of our home like my dad’s cigarette smoke, clinging to the carpet and furniture as a constant reminder.

I never expected an inheritance nor wanted one. After I became successful, I took care of my mother, buying a house for her to live in, a car to drive, and paying many of her bills. Toward the end of her life, after she spent her nest egg on nursing home care, I took over those expenses, too.

When she died in 2020, I paid for the funeral, and I thought that would be the end of all financial matters. However, she had one last surprise: I collected a $30,000 life insurance policy the following year. I didn’t know what to do with it, so it sat on my desk for a long time before I deposited it, a painful reminder of her passing.

My mother never owned a stock in her life, keeping her meager savings in a checking account and a few CDs. Since my mother was an educator, I decided it would be fitting to have her life insurance money, her final gift to her grandchildren, be used to teach them about investing in the stock market.

Invest in What You Know

In May 2022, when my children were 9, 8, and 5, I decided it was time to start their financial education. I taught them that investing in stocks was the same as buying a small piece of the company. They thought it was cool that I owned part of Apple since they were familiar with the company’s products in our house. I explained index funds to them, but that is a difficult concept for children to fully grasp. They were more interested in buying individual company stocks.

I let them each choose a stock to buy, with the caveat that they should consider what company they want to own for the next five years. We would only look at how the stock was doing once a year, but we would stick to their decision for at least 5 years.

My oldest son chose Tesla, which made sense. I love cars and talk about them often with my wife and kids. In 2022, it seemed like everyone in Austin was driving a Tesla, including half of the parents at his school. I gently discussed some of the problems I saw with Tesla as an investment, but to him, there was no way that Tesla wouldn’t be bigger in 5 years. I didn’t want to dissuade him, so we went with it.

My younger son went with Amazon since he saw their boxes show up at our house and homes around our neighborhood every day. To kids today, the Amazon truck must seem like the milkman, mailman, UPS, and Schwann truck driver all mixed together.

My daughter decided on Google. She understood that we always “Google” things when we wanted to know what it was. At five years old, she didn’t understand how they made money, but I thought it was a fair choice anyway.

The Purchase

On May 6, 2022, I purchased the stocks they chose in my online brokerage account. I only purchased one share of Amazon, which was trading at over $2,400 per share at the time. I then bought a roughly equivalent amount of the other stocks.

| Child | Stock | Date | # Shares | Price Paid | Total Value |

| 1 | Amazon (AMZN) | 5/6/2022 | 1 | $2,404.19 | $2,404.19 |

| 2 | Google (GOOG) | 5/6/2022 | 1 | $2,280.78 | $2,280.78 |

| 3 | Tesla (TSLA) | 5/6/2022 | 3 | $758.26 | $2,274.78 |

To mitigate the risk of investing in individual stocks, I subtracted the total value of each purchase from the $10,000 each child received from their grandmother and spent the remainder on shares of the Vanguard total U.S. stock market ETF (VTI).

| Child | Stock | Date | # Shares | Price Paid | Total Value |

| 1 | VTI | 5/6/2022 | 36.88 | $205.95 | $7,595.81 |

| 2 | VTI | 5/6/2022 | 37.48 | $205.95 | $7,719.22 |

| 3 | VTI | 5/6/2022 | 37.51 | $205.95 | $7,725.22 |

A Wild Ride in 18 Months

Oddly, all three companies have undergone a stock split since I purchased them. Amazon did a 20:1 stock split in June 2022, Google a 20:1 in July 2022, and Tesla a 3:1 in August 2022. Below are the purchase prices adjusted for stock splits.

| Child | Stock | Date | # Shares | Price Paid | Total Value |

| 1 | Amazon (AMZN) | 5/6/2022 | 20 | $120.21 | $2,404.19 |

| 2 | Google (GOOG) | 5/6/2022 | 20 | $114.04 | $2,280.78 |

| 3 | Tesla (TSLA) | 5/6/2022 | 9 | $252.75 | $2,274.78 |

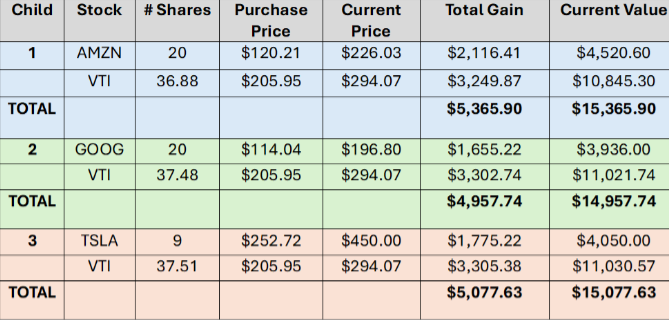

The stock price of these companies has taken a wild ride during the past 18 months. Amazon has been as low as $84.00 and as high as $232.93, Google between $86.70 and $198.16, while Tesla has unsurprisingly been the most volatile, with a value between $113.06 and $479.86. VTI was as low as $179.47 and as high as $302.45. Fortunately, each stock was higher on the day my kids wanted to look at their stocks, December 27, 2024, than at the time of purchase. I was able to show them portfolios that look like this.

This market volatility demonstrated some important lessons that I was able to discuss with my children.

Lessons Learned

Lesson #1: You can’t time the market.

Five weeks after purchasing the shares, the total stock market index was down nearly 11%. At some point during the past 18 months, Amazon and Google each lost 25% of their value, while Tesla was down over 60%! You could argue that we picked a terrible time to buy, but the portfolios are currently up 50%. The best time to buy is when you have the money. Over the long term, it won’t matter.

Lesson #2: Buy for the Long Term.

My children’s time horizon for these stocks, especially VTI, may be as long as 60 years! When you invest for the long term, there is no reason to check your stocks frequently. The price of all three individual stocks dropped almost immediately. Amazon didn’t regain our purchase price for 8 months, while it took Google one year and Tesla until November 2024! However, since we never looked at them (or at least the kids didn’t) during that timeframe, we never had the urge to sell and miss out on the recovery.

Lesson #3: Diversification is Important.

Individual stocks are more volatile than a diversified index. Each individual stock was down at least 25% during this holding period, and now they are all up at least 72%, but it could have very easily gone the other way. VTI dropped less and rose less. There are more stocks to help smooth out the ride with a diversified index.

Future Value

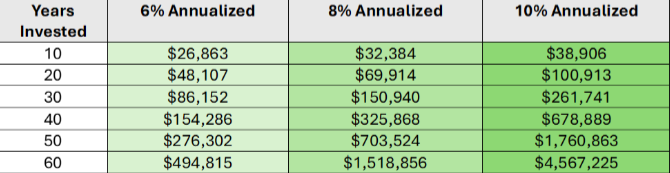

While $15,000 is a lot of money for a child, it isn’t going to change their lives . . . yet. However, compounded at 8% interest for 60 years, it would grow to more than 1.5 million dollars. More realistically, they may hold the stock for 10, 20, or 30 years, which would still give them quite a little nest egg.

Account Structure

The children’s portfolio is currently mixed in with my after-tax brokerage account. I have kept track of their shares separately, as I own additional shares of Google and Amazon. Fortunately, none of these three individual stocks pay dividends, making keeping track easier. VTI does, and I will have to account for that at some point when I transfer the money to their own accounts.

Several investment account options for children might be better: a 529 Plan, a Roth IRA, a custodial brokerage account (UGMA/UTMA), or a Trust. I will explore these in a future post.

Legacy

In ten years, my daughter will be 17. Maybe she’ll want to use the money to buy a slightly used car to get to her first part-time job, replicating the hard work her grandmother was capable of. In 20 years, my oldest son will be 31. Perhaps he’ll use the money as a down payment on a starter home, demonstrating the same foresight my mother demonstrated when she talked my father into buying their first and only house in 1969. In 30 years, my middle son will be approaching 40. He may use the money to fund a 529 for his children, ensuring her generosity extends to the next generation. Who knows? I will guide my children to use the money for a special purpose, one that creates a tangible benefit to their lives befitting their grandmother’s legacy.

The future is unknown and unknowable. There is no guarantee that this gift will grow more than it already has. However, we invest because we believe in tomorrow. We trust that the American economy will continue to innovate and thrive. We know that we will work hard to ensure future opportunities for our children, just as ours did for us. My parents helped me become who I am today, and their values flow through me to their grandchildren, setting the stage for them to achieve whatever goals they set for themselves.

I like the idea that my mother, who was born in a shack without indoor plumbing in 1937, who cooked breakfast for her brothers and then picked cotton in the West Texas sun, who married a coal miner and raised two kids in an 800 sq ft house, will someday be responsible for allowing her grandchildren to purchase their first homes. That is the power of investing, of compound interest, of generational skipping gifts. That is the power of a grandmother’s love.

Thank you for reading Business is the Best Medicine. Please subscribe to receive our weekly email. If you like this post, please share it on your social accounts. Thanks.