As you may have heard or (hopefully) noticed in your investment accounts, the U.S. stock market has been on a tear in 2024. The S&P 500 is up nearly 27% YTD, while the NASDAQ is up over 32%! While this is exciting for anyone invested in the market, it leaves a capital gains problem for those invested in post-tax brokerage accounts.

Capital gains are the money you make when you sell an asset for more than you paid for it. Yes, the government taxes you again on appreciation even though you have already paid taxes on the money you used to purchase the asset. Until you sell an asset, the gains are “unrealized.” Fortunately, you only pay taxes when you sell the asset and “realize” the gains. There are two types of capital gains: short-term, which are gains on investments held for one year or less, and long-term, which are gains on investments held over one year. Short-term capital gains are taxed as ordinary income, while long-term gains are preferentially taxed through a graduated system with three tiers (0%, 15%, and 20%) based on your taxable income.

Capital Gains Tax Rates

| Year | Filing Status | 0% | 15% | 20% |

| 2024 | Single | $0 – $47,025 | $47,026 – $518,900 | >$518,900 |

| 2024 | Married Filing Jointly | $0 – $94,050 | $48,351 – $583,750 | >$583,750 |

| 2025 | Single | $0 – $48,350 | $94,051 – $533,400 | >$533,400 |

| 2025 | Married Filing Jointly | $0 – $96,700 | $96,701 – $600,050 | >$600,050 |

These brackets differ from those used for calculating income tax on ordinary income. Read “Taxes: The Inescapable Bane of Medical Professionals” for an overview of the U.S. income tax system.

A capital loss occurs when you sell an asset for less than you paid for it and can be used to offset passive income. Tax-loss harvesting involves selling stocks that have decreased in value in order to capture the loss, then repurchasing the same stock one month later, or more commonly, purchasing a similar stock instead. While tax loss harvesting is often discussed in personal financial circles, it only works if you have a loss, which may be hard to find with the S&P 500 up dramatically this year. A lesser-known strategy that can reduce your future taxes and can be employed when the stock market is booming is tax-gain harvesting.

Tax-gain harvesting involves selling appreciated stocks in your taxable accounts and letting the government tax you on them . . . . at 0%! Unlike tax-loss harvesting, where you must wait 30 days to repurchase the same stock, there is no “wash sale rule” for capital gains. You can immediately repurchase the stock, reset your basis at the current price, and wipe out the capital gains.

Most physicians cannot utilize this strategy since the 0% capital gains bracket threshold is $94,050 in 2024 for married couples. However, married APPs may be able to take advantage, even with gross incomes significantly higher than this amount. In fact, married couples over 50 who both work may be able to utilize this strategy in 2025 with a gross income as high as $197,200 or more! Let’s review how taxable income is calculated.

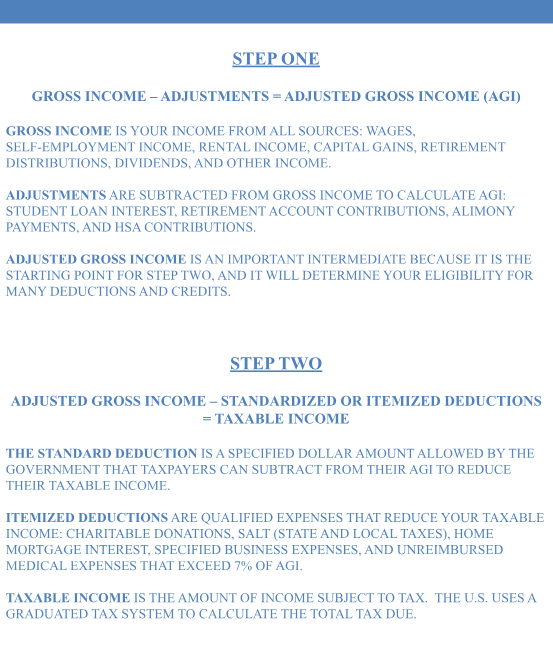

By understanding how the government calculates taxable income, you can see that APPs may make several adjustments to get under the 0% capital gains threshold. First, retirement account and HSA contributions are adjusted from gross income. While eligibility for HSA contributions varies, nearly all APPs have access to a 401k or 403b plan. Maxing out these accounts is not only high on the Financial Vitals Checklist but also helps you reduce your AGI. Additionally, many APPs make payments on student loans and can adjust off the interest portion. Finally, since most APPs are employees, they will take the standard deduction. Check out The Myth of the Tax Write-Off for a primer on standard vs. itemized deductions. Let’s look at some examples to understand how to perform capital gains harvesting.

Example 1

Blaine is a 57-year-old divorced physician assistant who earns $110,000 annually, including his salary and dividend income from his taxable stock portfolio. He had a late-career change and has worked as a PA for 7 years. Blaine lives frugally and maxed out his 401K in 2024, contributing $30,500 ($23,000 limit + $7,500 extra for being over 50). He has an HSA and contributed $3,000 for the year. He also paid $6,000 in student loan interest. He takes the standard deduction of $14,600. Additionally, he pays his ex-wife $12,000 alimony annually on an arrangement established before 2018, leaving these payments tax-deductible.

Gross income $110,000

– Adjustments $51,500 (401k, student loan interest, & alimony payments)

= AGI $58,500

– Standard Deduction $14,600

= Taxable Income $43,900

Blaine has a taxable income of only $43,900, which is below the 0% capital gains threshold for single individuals by $3,125. Blaine can take advantage of capital gains harvesting in his brokerage account. He owns $128,265 of VTI in an E-Trade brokerage account that he purchased prior to his divorce during his first career. Blaine wisely dollar-cost-averaged around $2,000 per year into this broad-based, low-cost ETF by Vanguard. He stopped when he got divorced, but the power of compound interest has been working for him in the 12 years since. His initial investment of $24,037 now has an unrealized capital gain of $104,228.

Many (but not all) stock trading platforms will allow you to choose which “lot” of stocks to sell. In capital gain harvesting, you want to select the shares with the lowest price paid, or “basis.” Blaine is subscribed to Business Is the Best Medicine and therefore knows this, selling 12 shares of his 2009 lot to realize $3,117.60 of capital gains.

Blaine then repurchases 12 shares of VTI for $3,621.60 at $301.80 per share, which is his basis in the new lot. The net result is that he has the same number of shares and total value and can continue to enjoy compound interest for years to come. In the process, he has made $3,117.60 of capital gains simply disappear.

As you can see from this example, it takes a lot of adjustments for a single APP to get below the 0% capital gains tax threshold. So many, in fact, that it will only work in a few extreme cases like Blaine’s. However, the following example demonstrates that for married APPs, it becomes a lot more applicable.

Example 2

Cindy is a married physician assistant who made $120,000 in 2024 and whose spouse is a stay-at-home dad. She contributes $15,000 to her 401K and does not have access to an HSA. Cindy paid $8,000 in student loan interest and took the standard deduction of $29,200.

Gross income $120,000

– Adjustments $23,000 (401k, student loan interest)

= AGI $97,000

– Standard Deduction $29,200

= Taxable Income $67,800

Cindy is $26,250 below the married filing jointly threshold for 0% capital gains. She owns 300 shares of CAVA at $33.34/share in her taxable brokerage account that she purchased one year ago. Her basis is $10,002, and the current value is $150.88/share, or $45,264.

Cindy has an unrealized capital gain of $35,264. She can sell 223 shares for $33,646, realizing a capital gain of $26,211.42.

If Cindy repurchases all 223 shares for the same price, she will now own 77 shares with a basis of $33.34 and 223 shares with a basis of $150.88.

Example 3

Janet, a nurse practitioner, makes $95,000 annually, while her husband, John, earns $75,000 as a mechanic. They both max out their 401k plans, contributing $23,000 each. They are both over 50, so they were able to contribute an additional $7,500 each. Janet has paid off her student loans and they take the standard deduction.

Gross income $170,000

– Adjustments $61,000

= AGI $109,000

– Standard Deduction $29,200

= Taxable Income $79,800

Janet’s family is $14,250 under the 2024 0% capital gains rate threshold. They own 225 shares of VTI in a taxable brokerage account, currently valued at $67,905.00. Their basis in this total stock market ETF is as follows:

They have an unrealized capital gain of $28,024, $14,250 of which they can use for tax-gain harvesting. They will want to sell the shares with the lowest price basis as follows:

The couple sold a total of 84 shares for $25,351.20. After the sale, they immediately repurchased 84 shares of VTI for $25,351.20, leaving their portfolio with the same number of shares and current value but less unrealized capital gains.

So, What’s the Point?

Unlike tax-loss harvesting, there is no immediate benefit if you buy back the shares you sold. You don’t have any more money in your investment account or pocket, and you won’t pay any less taxes this year. So, what’s the point?

Capital gains harvesting allows you to “bank” a tax win today for future use. While you don’t pay less tax today, the goal is to save you money in the future. As long-term investors, we believe that we will have substantial capital gains in the future. We also believe that our incomes will rise over time. Increasing the basis in the stocks we own today lowers our future capital gains tax.

In Example 1, Blaine raised his basis by $3,117.60. Once he pays off his student loan debt and his alimony payments cease, he will be in the 15% capital gains tax bracket, even if he continues to invest aggressively in his pre-tax retirement accounts. When he sells his shares, he will save 15% of $3,117.60, or $467.64.

In Example 2, Cindy removed $26,211.42 of capital gains from her portfolio. Once their kids start school, her spouse will start working again, putting them into the 15% capital gains tax bracket. If they sell their shares at that time, they will have saved $3,931.71 in taxes.

In Example 3, Janet and her husband harvested $14,250 in capital gains. Unfortunately, unexpected expenses prevent them from maxing out their retirement plans in a few years, pushing them above the 15% capital gains tax threshold. Fortunately, they can sell shares of VTI to raise money and save $2,137.50 in taxes on the sale.

As you can see from all three examples, the capital gains they harvested in 2024 will help them in the future when their circumstances change.

The Market Doesn’t Have to Be Up to Employ this Strategy

I started this article discussing the hot U.S. stock market in 2024 because even new investors are now likely sitting on some capital gains. However, long-term investors can apply this strategy even in a down year. Let’s look again at Blaine’s brokerage account holdings from Example 1.

If the U.S. stock market broadly loses 20% in 2025, VTI, as a total market ETF, should also lose 20%. That would leave the price per share at $241.44. Every share that Blaine purchased before 2024 still has an unrealized capital gain, which can be harvested if his financial situation remains unchanged. You can employ this strategy whether the stock market is up or down as long as the basis in your shares is below the current market price and you have room in your taxable income before you reach the 0% capital gains threshold.

How to Get Started

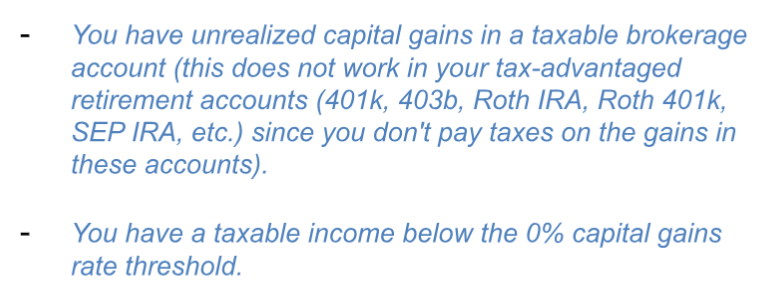

In order to perform capital gains harvesting, the following must be true.

If these two statements are true, follow this step-by-step guide.

- Go to your brokerage account and identify any stocks you purchased over a year ago. You have long-term capital gains if the purchase price was less than the current value!

- Calculate your taxable income using the method presented above.

- If you fall into the 0% capital gains tax bracket, calculate how much room you have until you reach the threshold.

- Realize the capital gains by selling the shares you identified in Step 1 until you run out of capital gains or reach the threshold calculated in Step 3, whichever comes first.

- Repurchase the shares you just sold. You must claim these gains on your taxes, which will be taxed at 0%. You have now completed capital gains harvesting!

Conclusion

I hope this article has simplified capital gains harvesting. While not every medical professional will be eligible, plenty of use cases exist, especially among married Nurse Practitioners and Physician Assistants. Think of capital gain harvesting like putting some tax-free money back into your brokerage account for future use.

While the benefit from any one year is unlikely to be substantial, this strategy can be used repeatedly, giving you a tax-free bucket of money from which to pull when it is advantageous to you. In personal finance, we are playing the long game, and capital gains harvesting is another tool that can help you win the ultimate prize – financial freedom!

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]