As medical professionals, your greatest advantage in real estate investing can also be your biggest limitation. A W2 job is great for buying power and your ability to borrow money, but it also means your time is limited. Real estate investing often conjures images of late-night phone calls, chasing down rent payments, fixing leaky toilets, and dealing with unruly tenants. As busy, high-earning medical professionals, who has time for that? However, real estate investing doesn’t have to be time-consuming—you don’t have to be a landlord or flip houses yourself. Let me show you how to make money in real estate without managing properties daily.

At Business is the Best Medicine, we recommend following the Financial Vitals Checklist. Steps 1-4 are vital to your financial success, so protect yourself, maximize your returns, and secure your retirement before investing in real estate. Use the Basics series to review these steps and make your financial plan.

This article is for you once you’ve checked off these steps and are ready to start building wealth through asset accumulation. While Dr. Slater’s article on how to get wealthy provides a variety of asset options, here, I’ll focus on five real estate strategies that can work even with a busy schedule:

1. Short-Term Lending

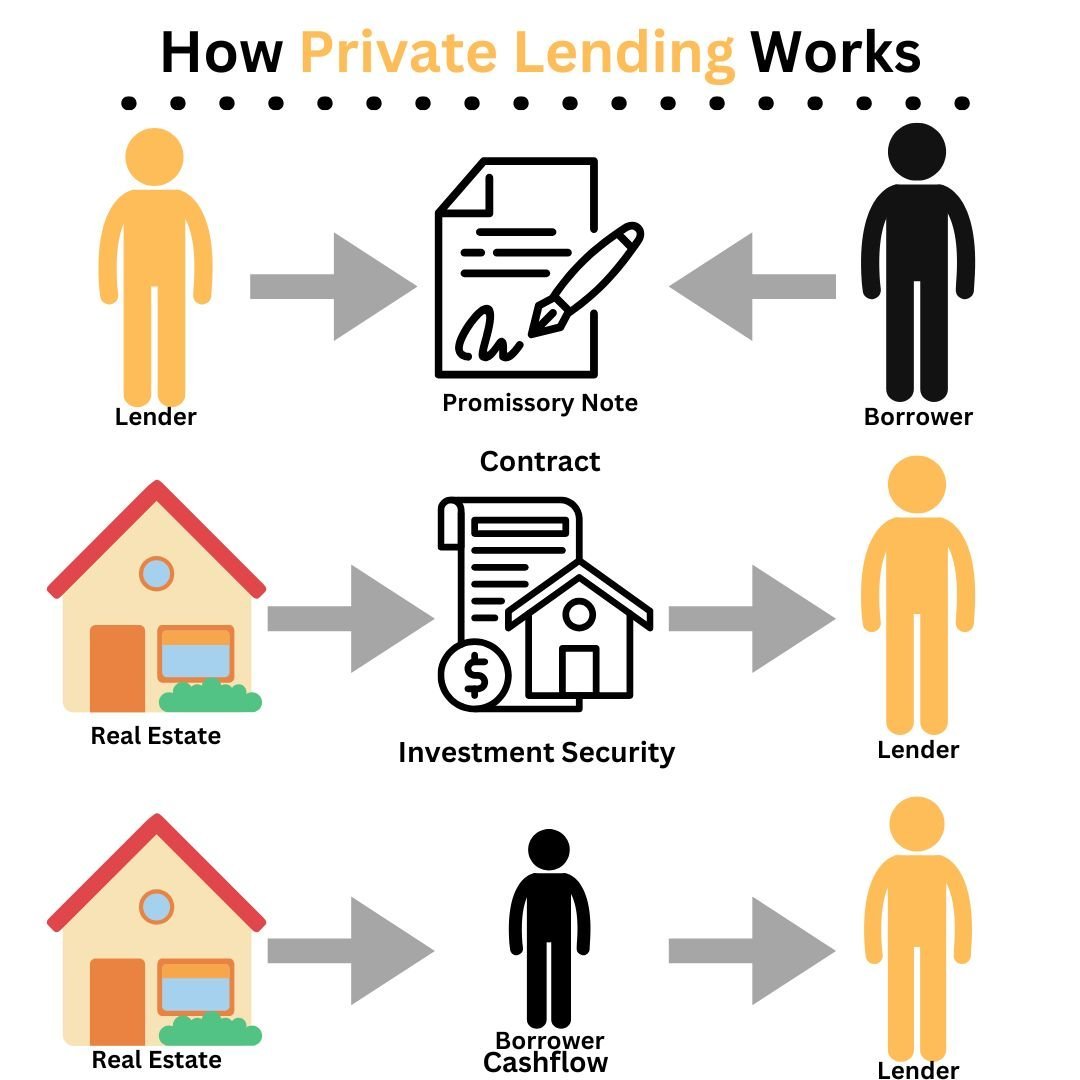

Short-term lending involves providing funds to real estate investors for quick-turnaround transactions, and it can be a highly lucrative way to invest in real estate with minimal time commitment. There are two primary types of short-term lending:

- Earnest Money Deposit (EMD) Lending:

In real estate, an earnest money deposit is the money provided to a title company to open escrow on a property. This deposit demonstrates the buyer’s intent to purchase the property. As an EMD lender, you loan this money to an investor, and your funds are typically returned within 30-45 days when escrow closes. Returns can be substantial, often up to 25%, and sometimes even higher. For example, I’ve lent $2,500 on smaller deals and received $5,000 back when escrow closed.

- Transactional Lending:

This type of lending involves providing funds to an investor who is buying a property and plans to sell it quickly—sometimes the same day or the next day. This is what we call a “double close.” The original buyer closes on the property twice. For instance, Investor B might purchase a property for $100,000 (A-to-B transaction) and sell it the same day or within a few days for $200,000 to Investor C (B-to-C transaction). As a transactional lender, you fund the A-to-B purchase, which is repaid once the B-to-C transaction closes. This usually happens within a few days, making it an incredibly short-term commitment.

Who Are You Lending To, and Why?

In EMD and transactional lending, you typically lend to wholesalers or seasoned real estate investors who operate high volumes of deals. These investors often choose to use other people’s money for several reasons:

- Preserving Capital for Other Deals: Investors may be involved in multiple transactions simultaneously and prefer to avoid tying up their funds in escrow for 30-45 days.

- Scaling Their Business: By using other people’s money, investors can increase their deal volume without depleting their capital reserves.

- Cash Flow Optimization: While they pay slightly more to borrow from private lenders, their ability to close more deals at scale offsets this cost.

These investors are typically experienced and reliable, ensuring your money is secure with clear contracts and maintaining timelines.

What Are the Risks and Protections?

While the potential returns are high (12-15% for transactional lending and 25% or higher for smaller EMD deals), it’s essential to mitigate risks by:

- Having Proper Contracts in Place: Your funds should be protected in escrow or by contract outlining the repayment terms.

- Monitoring Deadlines: For EMD lending, stay on top of inspection periods to ensure your funds are refunded if the buyer cancels the deal. You protect your investment by ensuring you retrieve your funds before they go “hard” (non-refundable).

- Verifying the Investor’s Track Record: Work with seasoned investors with a successful history of closing deals.

Short-term lending is an excellent way to diversify your investments, especially if you want consistent, quick returns without managing properties. By partnering with experienced investors, you can make your money work for you while staying focused on your career.

2. Long-Term Lending

Long-term lending is another great option for busy professionals looking to generate passive income through real estate. This strategy typically involves lending money for 3+ years, providing steady, predictable returns.

Who Are the Borrowers?

In these instances, you’re lending to seasoned investors, not newbies. These investors operate at scale, handling multiple deals and projects, and they use other people’s money to continue growing their businesses without tying up their capital. Like short-term lending, these borrowers prioritize deal volume and leverage external funds to maximize their opportunities.

What Are They Doing With the Money?

Most of the time, you’ll be lending the down payment (typically 20% of the purchase price) for a property or renovation costs associated with a purchase or rental. Your funds remain invested in the property for a longer period, generally 3-5 years. During this time, the borrower uses the funds to:

- Purchase the property

- Renovate or improve it to increase value (if applicable)

- Stabilize the property through leasing or other strategies to generate cash flow

At the end of the loan term, the borrower will either:

- Pay you back in cash (from profits or savings)

- Refinance the property to pay off your loan

- Sell the property to repay your loan and generate their own return

What Are the Benefits?

- Less Risk: Unlike short-term lending, long-term lending is generally less risky because a lien on the property secures your investment. This lien is typically in second or third position, ensuring your claim on the property is legally documented.

- Predictable Returns: You’ll earn interest on your investment, which can be paid monthly, quarterly, or annually—depending on the agreement. This creates a steady income stream, often called “mailbox money.”

- No Need to Reinvest Constantly: Long-term lending is ideal for investors who don’t want to spend time finding new deals repeatedly. Instead, you can park your money in a single deal and let it grow over a longer period.

This method is perfect for those who prefer a hands-off approach and are looking for steady returns with lower risks. By partnering with experienced investors, you can benefit from their expertise while making your money work for you consistently and reliably.

3. Turnkey Rentals

Turnkey rentals are newly built or recently renovated properties ready to rent immediately. This approach reduces your time and effort because the property requires little maintenance. There are two common paths:

New Builds: Companies like DR Horton offer mass-produced homes with 1–2 year warranties, making them ideal for low-maintenance rentals. You can manage the property yourself or hire a property manager.

Full-Service Turnkey Providers: Companies like REI Nation handle everything—from purchasing and renovating homes to tenant placement and ongoing property management. This option is truly hands-off, albeit at a slightly higher cost.

Turnkey rentals are a great way to own rental properties without the hassle of in-depth renovations or older properties that usually require more repairs.

4. Wrap Deals

Wrap deals and lease options are creative financing strategies that allow you to profit from real estate without taking on the responsibilities of a traditional landlord. Both options involve structuring the sale of a property to a buyer in a way that generates income while minimizing your involvement in property maintenance.

Option 1: Wrap Deals

In a wrap deal, you purchase a property in cash or through seller financing from the original owner. You then “wrap” the deal by reselling the property to an end buyer at a higher purchase price, with a higher interest rate, and structured monthly payments that cover your costs and provide a profit. If you purchased the property using seller financing, part of the buyer’s monthly payment will go toward paying the original seller, while the remainder becomes your profit.

Key Requirements for Wrap Deals:

- You need to vet the buyer thoroughly to minimize the risk of default.

- Understanding the local laws is critical, as some areas have legal restrictions or specific requirements for wrapping a purchase.

- You must use the correct contracts and work with a knowledgeable title company to protect your investment and ensure legal compliance.

Why It’s Less Work Than Being a Landlord: - Unlike traditional rental properties, the buyer is responsible for maintaining the property as they purchase the home from you. You no longer have to worry about leaky toilets, property repairs, or ongoing maintenance because the buyer owns the home. If the buyer defaults, you regain ownership and can resell the property.

Option 2: Lease Option

A lease option is similar but offers more control. In this strategy, you maintain ownership of the property and lease it to a tenant-buyer under an agreement allowing them to purchase the home after a set period.

How It Works:

-

During the lease period, you retain ownership, but the tenant-buyer treats the property as their own.

-

You buy the property in cash, through seller financing, or with a mortgage.

- You lease the property to the tenant-buyer, who agrees to terms that allow them to purchase the property in the future.

- Why Lease Options Can Be Better:

Lease options allow you to maintain property ownership until the sale is completed, giving you more control and protection. Additionally, because the tenant-buyer is working toward ownership, they are typically more invested in taking care of the property than a traditional renter.

Why These Strategies Are Less Work Than Being a Traditional Landlord

- Buyer Motivation: Buyers typically work toward homeownership in both wraps and lease options. This means they are more likely to take care of the property and less likely to call you for minor issues.

- Limited Maintenance Responsibilities:

- In wrap deals, you do not maintain the property since the buyer assumes ownership.

- In lease options, you may have some maintenance responsibilities initially, but these are typically short-term since the tenant-buyer intends to purchase the property.

- Fewer Tenant Issues: Because the end goal is ownership, buyers are more likely to stay long-term and make payments on time.

What to Watch Out For

Both strategies require upfront effort to:

-

Vet Buyers: Ensure they have the financial capability and commitment to follow through with the terms.

- Understand Contracts: Use proper documentation to protect yourself legally.

- Partner with a Reliable Title Company: Ensure compliance with local laws and minimize risks, especially for wrap deals.

While these strategies require a bit of groundwork, they can significantly reduce the ongoing work associated with traditional landlord duties, offering a profitable and less stressful way to invest in real estate.

5. REITs and Syndications

While owning homes or buying properties directly can yield high returns, it often involves significant time and effort. Options like short-term lending, long-term lending, turnkey rentals, or wrap deals are less intensive than managing a rental portfolio but still require some involvement, such as monitoring contracts or vetting borrowers. If you’re looking for the most hands-off approach, Real Estate Investment Trusts (REITs) or syndications are ideal.

REITs

REITs are publicly traded companies that own or finance real estate across various asset classes. They are highly liquid, easy to access, and allow you to invest with minimal capital and effort. With professional management and regulatory oversight, REITs provide a simple way to diversify into real estate without hands-on involvement.

Syndications

Syndications, on the other hand, pool funds from multiple investors to purchase larger properties, such as multifamily complexes or commercial buildings. While they often offer higher returns than REITs, syndications carry certain risks:

- Reliance on the Syndicator: The success of the investment depends heavily on the syndicator (general partner) who manages the project. A poorly managed syndication can lead to lower returns or even losses, so choosing a reputable and experienced syndicator is crucial.

- Lack of Diversification: Unlike REITs, which spread investments across multiple properties and markets, syndications typically focus on a single property or project. This concentration increases your exposure to risks tied to that specific asset.

- Illiquidity: Your funds are locked in for 3-7 years, meaning you won’t have access to your capital until the property is sold or refinanced.

- Market and Economic Risks: Syndications are sensitive to market conditions, interest rate changes, and local economic factors, which can all impact returns.

Despite these risks, syndications can be highly rewarding for investors with larger capital to deploy and a willingness to lock their money away. By partnering with a skilled syndicator and thoroughly reviewing the deal’s structure, you can mitigate risks and enjoy higher returns with minimal day-to-day involvement.

Both REITs and syndications allow busy professionals to invest in real estate without managing properties or tenants. REITs are ideal for those seeking liquidity and diversification, while syndications cater to those comfortable with higher risks and long-term commitments in exchange for potentially higher returns.

REITs vs Syndications

| Criteria | REITs | Syndications |

| Returns | 8-12% annually, tied to market performance | 15-20% annually, including cash flow and appreciation |

| Liquidity | High – easily bought/sold on the stock market | Low – funds are locked for 3-7 years |

| Risk and Volatility | Higher due to stock market volatility | Lower volatility; tied to property/project performance |

| Management | Professionally managed; no control over specific properties | Direct interest in specific properties; no active management required |

| Accessibility | Highly accessible; low entry barriers ($100-$1,000+) | Requires larger investments ($25,000–$100,000+) |

Conclusion

Real estate investing doesn’t have to involve leaky toilets, chasing tenants for rent, or flipping houses on weekends. There are many ways to generate wealth through real estate without becoming a traditional landlord or sacrificing your busy schedule. Options like short-term lending, transactional lending, or wrap deals let you earn substantial returns by leveraging your capital and partnering with experienced investors. For those with more time and resources, turnkey rentals provide a low-maintenance way to build a portfolio. For the most hands-off approach, syndications and REITs offer passive income opportunities with varying levels of involvement and risk.

Real estate investing with a busy schedule is entirely possible. Whether you’re leveraging your expertise as a lender, building relationships with seasoned investors, or parking funds in REITs or syndications, the right strategy will depend on your goals, risk tolerance, and available time. The key is to focus on strategies that align with your resources and to build trusted partnerships along the way. With the right approach, you can diversify your income streams, achieve financial growth, and secure your future—all without compromising your career or personal life.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]