Personal Finance for Medical Professionals Part I

Welcome to Personal Finance for Medical Professionals, a series of articles designed to introduce you to the basic principles of personal finance and investing. I have used similar material in lectures to residents, fellows, and students for several years. You will now have access to this information from the comfort of your computer screen, with the added bonus of not having to listen to me talk. This series will give you a solid foundation on which to build your financial life. This series is intended for medical residents, fellows, new attendings, or anyone who wants to understand how money and investing work. Let’s get started with Part I, Lesson One.

Why Medical Professionals?

Medical professionals come from all walks of life. We all have a unique backstory, including our relationship with money; some of us grew up rich while others were poor. In the same medical school class, you may have the daughter of an investment banker and the son of a coal miner. These two students likely grew up with very different ideas and feelings about money.

Education is the great equalizer. Regardless of family history and socioeconomic status, everyone studies the same material to graduate as highly paid medical professionals. However, nowhere in the medical school curriculum does it teach us HOW to deal with this high income.

I am a perfect example of this lack of financial education. I graduated from my Residency in Emergency Medicine without ever taking a class about personal finance—not one class in over 20 years of formal education! Unfortunately, this is not uncommon. Whether by oversight or design, the education system in the US does not include how to manage your finances.

Although this is slowly changing due to the efforts of those in the FI community, it is currently up to you, the medical professional, to learn about personal finance and how to manage your money. Fortunately, you are not alone. Business Is the Best Medicine is here to guide you through the process.

The Good, The Bad, and the Ugly

Most people believe that being a medical doctor or dentist puts you on the fast track to financial success. However, there are economic advantages and disadvantages to becoming a medical professional.

A high income is obviously the most significant advantage of the medical professional. The higher your income, the more money you can potentially save and invest. Another lesser-known advantage is having access to credit and leverage. Doctors can borrow money, often with little money down. This access to credit can be tremendously helpful if used to finance assets such as rental real estate or a personal business.

However, there are also financial drawbacks to becoming a physician. Many of us graduate with hundreds of thousands of dollars of student loan debt, often financed at medium to high interest rates. While most medical professionals get a good return on their investment in medical education, student loan debt can potentially hinder your personal finances for decades. Next, most doctors graduate from their residencies at around 30 years of age, with some being even older. As we will discuss in Part I, Lesson Two, an early start to investing is tremendously powerful, leaving medical professionals at a disadvantage from their relatively late start.

Some hidden pitfalls also tend to ensnare high-income doctors and dentists. While these are not exclusive to the medical community, they trap many of our colleagues. The first is social pressures around lifestyle. Everyone knows that doctors make a lot of money and often expect us to drive luxury sedans, wear expensive clothing, and live in “doctor mansions.” This pressure can come from family, colleagues, social media, and even our patients! Here, our access to credit is a double-edged sword. While it can be helpful to have access to loans if we buy assets, it can be financially devastating to use leverage to give into these social pressures and prematurely inflate our lifestyles.

Additionally, doctors are generally intelligent, hardworking, accomplished humans. While you might think this is an advantage, our overconfidence can lead us astray. As you will discover during this blog series, the best investors are those who don’t overthink! Finally, highly educated medical professionals innately trust those with authority and credentials. This can lead us to blindly trust financial advisors who may not have our best interests at heart.

Why Learn About Personal Finance?

Money struggles can affect anyone, regardless of income. Despite their high incomes, I know plenty of doctors living paycheck to paycheck. It isn’t that they aren’t making enough money; it’s that they aren’t managing it correctly.

My father worked in a coal mine and had a company pension. He never worried about retirement and never invested in stocks, bonds, or real estate. He thought it was all covered – until he died before age 50. My mother was left to return to work after 20 years as a full-time mom – things don’t always work out as planned. The sad part is that even if he had lived, the pension at his company would never have paid out all it promised, as it was later “restructured” due to lack of funding.

Medical professionals don’t have a pension, and many work as independent contractors who don’t even have access to a 401k! It is ultimately up to you to manage your financial life. No one will ever care more about your finances than you do.

You need to ensure that you have enough money to live, take care of your family, put your kids through college, and retire comfortably. This can seem like a daunting task. Fortunately, you have all the tools to handle the job—a high income, intelligence, the ability to defer gratification, and this blog series!

What is Personal Finance?

So, what is personal finance? It is how you think about and deal with money in all aspects of your life. It includes fundamental concepts that all medical professionals should know, habits they should develop, and financial milestones they should accomplish.

The topic encompasses education, action, and achievement, including basic budgeting, insurance, retirement planning, and the concept of financial independence. Everyone deals with money, though most do it haphazardly without intention or optimization. Studying personal finance is a lifelong journey that allows us to optimize the use of money to improve our lives.

Introduction to Basic Concepts of Personal Finance

Gross Income – The total amount you earn from your job before any taxes.

Net Income – The amount you earn after taxes and any job-related expenses.

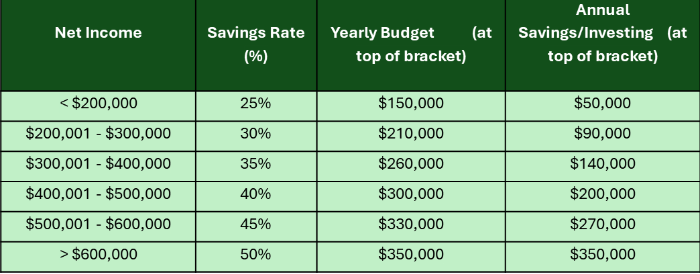

Savings Rate—The percentage of net income you hold back to save/invest. A high savings rate is essential for those in control of their finances.

Let’s assume that you are an ER doctor with a monthly gross income of $40,000. As an independent contractor living in a state with income tax, you assume a 35% total tax burden. For a primer on taxes, click here. Therefore, your net income is $26,000 a month. If you save $9,100 per month, your savings rate is 35%.

I believe all physicians should save AT LEAST 25% of their net income, and their savings rate should increase as their income increases. For example:

These percentages should be the minimum that you save. Start by calculating your net income, then set your savings rate. This will tell you how much money is left for you to spend. Unfortunately, most people do this backwards by spending what they want and saving what is left (if anything). However, we approach our money intentionally.

Budget – Your spending plan for a designated pay period.

A budget contains essential items such as housing, transportation, and food, as well as non-essential items such as travel and entertainment. You want to keep the cost of your essential items as low as possible, as these items are often fixed (mortgage payment) and constitute the bulk of your expenses.

Once you’ve calculated your minimum savings rate and set a spending budget, see if you can comfortably live on less than that amount. If you can save more aggressively, do it. Remember that your budget was set using your net income. If you bring home more than $600,000 after tax and can’t live off half of it, you have a spending problem!

Total Expenses – The amount of money you spend per period (month, year). Tracking your expenses is essential, as they will affect your retirement calculations.

Investment – An investment is a financial asset bought with the reasonable expectation that it will provide income or that it will later be sold for a profit.

Net Worth = Total Assets – Total Liabilities.

When you start your career as a medical professional, your net worth will likely be negative. This is because most of us have a large amount of student loans (a liability) and few assets. You must reverse that as quickly as possible. The best way to increase your net worth is to have a high savings rate and invest your money regularly.

To become financially independent, you want to accumulate assets that produce a return – preferably liquid assets like stocks and bonds or those that produce cash flow, like rental real estate or a small business.

Primary Residence – Your primary residence is the personal home in which you live.

You should avoid the “Doctor Mansion” at all costs. If you are starting a new job in a new town, buy the smallest, cheapest home in which you are comfortable. If you don’t like your job or get fired, can you rent it out? Can you even sell it? If you can’t, you will lose money on transaction fees or get stuck with two mortgages. If the job works out you can always buy a bigger house later.

The more money you spend on your primary residence, the less money you will have to save and invest. This will reduce your ability to accumulate income-producing assets. Not all assets are equal. An income-producing asset is an investment that you reasonably expect will produce cash flow and/or appreciation. A non-income-producing asset is one in which you do not.

While your personal home is an asset, it is not an investment. It does not produce income if you do not rent out part of it. The average American has most of their net worth tied up in their home. This gives you a false sense of how well you are doing financially. If your house has appreciated, your net worth is positive, but you can only access it by selling your home! Where will you live? Are you willing to move to a cheaper area, significantly downsize your home, or become a renter? If not, the equity in your personal residence isn’t useful. For this reason, many financial planners will tell you to ignore your primary residence when calculating your net worth.

Financial independence occurs when your accumulated assets earn enough income to fund your monthly expenses. At that point, you no longer have to work for a paycheck. This can be at traditional retirement age or earlier, depending on when this achievement occurs. I believe this should be the ultimate goal of every medical professional.

However, you don’t have to reach financial independence in order to benefit from building assets. Eventually, you will have enough assets to replace all of your income for a short period or some of your income for longer. You may decide to take a sabbatical, work less, or change careers. Becoming financially independent means you now have a degree of financial flexibility – the ability to make decisions without money being the primary factor. You can quit a job you don’t like or move to a new area. Freedom is the key word.

Final Thoughts

Medical professionals have a high income but also have some significant financial disadvantages, such as a late start and a high student loan burden. If we start our careers without studying personal finance, we may find ourselves trapped in a suboptimal job living month-to-month to support our spending habits.

Whether you’re interested in becoming financially independent as quickly as possible, retiring early, or simply avoiding the month-to-month trap, you must learn how to manage your money to reach that goal. This starts with three general principles that are easy to understand but take discipline to follow. These three principles are the focus of the next lesson, which can be found in Part I, Lesson Two.

Thank you for reading Business Is the Best Medicine. I hope you enjoyed this edition of Personal Finance Basics for Medical Professionals. Subscribe below so you don’t miss future installments of this series.