Welcome to Business Is the Best Medicine’s Personal Finance for Medical Professionals, Part I. In this series, we follow a curriculum designed to make you knowledgeable and confident enough to manage your hard-earned finances. If you haven’t already read Lesson One: Why Personal Finance?, please click here.

General Principles

In Lesson Two, you will learn three general principles. These principles seem simple, almost too basic. While they are easy to learn, they can be difficult to follow. Remember that knowledge without action is insufficient. You must understand and consistently apply these principles.

- Spend Less Than You Earn & Invest the Difference

- Start Early

- Know Your Goals & Make a Plan

1. Spend Less Than You Earn & Invest the Difference

If you only take one thing away from this entire blog series, make it this: the foundation of building wealth as a medical professional is to spend less than you earn and invest the difference. That’s it. Sounds simple, but it is deceptively hard.

Our entire economic system, capitalism, is based on the investment of capital. Spending less money than you earn at your job provides you with capital to invest. Invested capital, in turn, makes money for you. Once the funds you have invested produce enough returns to pay for your life, you’ve won capitalism. That’s how this game is played.

Unfortunately, our society celebrates consumption, as modeled by television, movies, and social media. We are inundated with images of luxury cars, expensive homes, and fancy clothes. YOLO permeates our culture, causing Americans, including physicians, to spend more money than they earn, leaving them without capital.

You must decide which team you will be on—Team Capitalism, which owns the businesses making the products and services, or Team Consumer, which buys those same products and services.

To be on Team Capitalism, you don’t have to start and own a business; you just need to invest in the stock market. When buying a stock, you become the owner of a small piece of a business, which entitles you to share in the company’s profits. When you spend less than you earn, you have the capital to purchase that ownership.

So, how much should you save and invest? In Part I, Lesson One, I outlined how to calculate your savings rate. I believe that all medical professionals should save at least 25% of their net income, and preferably more, depending on their income bracket. That sounds like a lot, but since a significant portion of this will be in pre-tax retirement accounts, it is very doable. I would have a different suggestion for a primary school teacher making $50,000 a year. But, as a medical professional with a high-paying career, this should be your goal.

The Golden Formula

Too many people feel they must win the lottery or start a successful internet business to become wealthy. Fortunately for American physicians (and their high incomes), getting wealthy is formulaic . . . in fact, I have the formula:

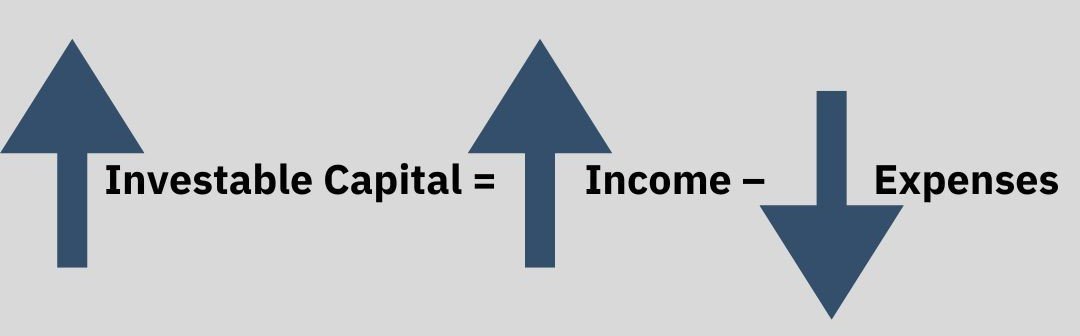

Investable Capital = Income – Expenses

This is a formulaic representation of our mantra, “Spend less than you earn and invest the difference.” Your income minus your expenses equals the money you can use as capital to save or invest. Visualizing this formula is important because, like other formulas, manipulating the variables changes the outcome.

If you earn more money while holding expenses the same, you have more investable capital. If you lower your expenses while keeping your income fixed, you will also have more capital. And, if you do both, you can supercharge the amount you can save and invest.

Most doctors don’t have an income problem; they have a spending problem. Thus, the fastest way for most medical professionals to increase their investable capital is to spend less money. Don’t buy a new car when you finish residency. Don’t buy a “doctor mansion.” Keep your expenses low so you have more capital to purchase assets that will make you money.

If you can work extra hours, especially at the beginning of your career, do it. The more you make and the less you spend early in your medical career, the better. In fact, it’s so important to start early that it’s General Principal #2.

Below are a few pictures demonstrating ways that I increased my income and decreased my expenses early in my career. I did a lot of work myself in order to build my real estate and urgent care businesses, and you better believe I invested the resulting capital!

2. Start Early

Investing early in your career gives you two significant advantages. First, it develops good financial habits. It is easier to make healthy eating a part of your lifestyle than eating whatever you want for ten years and then attempting to diet. Similarly, keeping your expenses low early in your career is easier, especially if you have just finished residency. You have been living off a resident’s salary, so you know you can live off a small, fixed amount. Additionally, you have been working resident hours. Keep doing that for the first 3-5 years of your career. This 1-2 combo allows you to supercharge your capital accumulation.

Now that you have some capital to invest, starting early gives you the second advantage – compound interest. It is imperative that you understand how powerful compound interest is, as it is the basis for your future wealth and retirement funds! With compound interest, you earn a return (interest) on the principal or amount you invest, PLUS you earn a return on the interest you have already earned. Compare this with simple interest, where you earn a return only on the principal only.

This chart teaches us two lessons. First, compound interest is powerful. With simple interest, a $1,000 investment would only produce a total of $5,000 (including the original capital) after 40 years. This is a 4X return on your capital. However, with compound interest, you would have $45,000, or a 44X return!

The second lesson is that compound interest takes time to work. For the first few years, there is hardly any difference. Even after year 10, the difference is minimal. However, in years 20, 30, 40, and beyond, the power of compound interest starts to become apparent.

This is why it is so important to start early. The earlier you start, the longer your money has to grow. In this example, every dollar you invest for 40 years becomes $45, while a dollar invested for 20 years is only worth $6.74. The more money you can invest during the first few years of your career, the better.

How does this translate into real life? Let’s compare three friends: The first started working right after college and invested $1,000 per month until retirement at age 67. The second went to medical school and began investing $2,000 a month immediately upon finishing residency. Finally, the third friend also went to medical school but waited until age 42 to start investing $4,000 per month. Who will have the most money at age 67, assuming an 8% annualized compounded rate of return?

Despite investing over twice as much capital, the friend who started at age 42 still ends up with $1,000,000 less than the friend who started at age 22. This clearly demonstrates the power of starting early and also shows that if you start later, you will have to invest significantly more capital in order to make up for lost time.

3. Know Your Goals & Make a Plan

Imagine driving down a highway with no idea where you were going. How would you know which way to turn? How would you know when to stop? If you are in Florida and want to drive to North Dakota but have limited fuel and no map, do you think you’ll get there? Living your life without a financial plan is similar. You need a destination and a financial roadmap.

Begin by figuring out your goals. What do you want out of your financial life? To drop dead at 80 in your office, still seeing patients because you never saved money for retirement? Perhaps instead, you want to retire at age 45. Either of these two disparate goals are fine if that’s what you really want, but just understand that the lifestyles you will lead and the maps that will take you there are very different.

We all are unique beings – some of us have families to care for, while others don’t. Some of us love our jobs and can’t imagine retirement, while others can’t wait to get out of medicine. Start by asking yourself a few questions:

- Do you want to retire early? If so, at what age?

- Do you want to stay home with your kids? Will you still work part-time or not?

- What kind of lifestyle are you willing to accept? Luxurious, Comfortable, or Basic?

- Will you pay for your kid(s)’ college?

- Do you want to travel? When? How? Do you want to fly coach or first class? Stay at the Mariott or the Four Seasons?

- Do you have parents/extended family to support?

- Is philanthropy important to you? How much do you want to leave?

- Do you want to create legacy wealth for your heirs?

There are no right or wrong answers to these questions, but your plan must be congruous with your goals. You can’t decide you want to retire early and then spend every dime you earn on a luxurious lifestyle and fancy vacations.

Putting It All Together

The final figure below visually represents how your financial life progresses in a capitalist system. As a new attending, you have no capital, so you should work as much as possible to produce some. You make more money by working more, but your cash flow is constant because you use that extra money to invest.

By the middle of your career, you have accumulated some capital that is working for you. You will not work as hard as you did at the beginning of your career, as you will be tired and have other responsibilities.

By the time you retire, you are not producing any income from your labor, but your capital should now make enough money to keep your cash flow unchanged. You used your labor to create capital, which has been invested to produce cash flow so you can eventually stop working.

Final Thoughts

As a medical professional, you are primed to win capitalism. You have already completed the most challenging part by obtaining a high-paying career that will provide you with excess money to use as capital. Congratulations! Now, you must use the three general principles to take advantage of your high income and take control of your financial future.

Spend less than you earn and invest the difference. Period. Calculate your net income, and then decide your savings rate. Don’t fret if you are already a few years into your career, as the best time to start anything is today. Today IS early compared to five years from now. It’s all relative. Just start. Finally, decide what you want from your life, make a plan, and go get it. Action is what will separate you from all those who wake up one day and fret over the fact that they have no control over their finances. Life isn’t a spectator sport. Put your helmet on and get in the game.

Lesson Three in this series, The Financial Vitals Checklist, provides a blueprint for success. We give you a step-by-step guide on how to proceed with your investable capital. You don’t have to get lucky; you just have to follow directions.

Thank you for reading Business Is the Best Medicine. I hope you enjoyed this edition of Personal Finance for Medical Professionals. Subscribe below so you don’t miss future installments of this series.