Introduction I just completed my annual personal financial statement. The bank that holds the loan on my largest commercial building requires me to turn it in at the beginning of every year. A personal financial statement (PFS) is like a net worth statement on steroids. It catalogs your assets and liabilities like a net worth statement while also documenting and projecting your income and expenses.

I have completed several slightly different statements for various banks over the years in order to receive loans for urgent care clinic buildouts and commercial property. I initially thought it was a tedious waste of my time. However, after completing one annually for several years, I now look forward to the exercise as it clearly documents my financial progress. Seeing my loan balances shrink while my investments grow over time is exciting and rewarding.

In this post, I will walk you through a fictitious PFS for Dr. John Smith and his wife, Jane. This PFS is a five-page Excel sheet you can update with any changes from year to year. I have modified it specifically for personal use by medical professionals. At the end of the post, I will provide a link where Business is the Best Medicine subscribers can download a free, blank copy of the PFS.

PAGE ONE

Part 1 – Personal Information

Your personal information goes on the top of page 1. This is information that a bank requires, so you can leave most of this blank if it is for personal use. I left it here in case you ever need to send it to a bank.

In this example, Dr. John Smith works as an ER physician, is in his fourth year out of residency, and is married with two children.

Part 2 – Net Worth Statement

This section lists your assets and your liabilities and calculates your net worth. Worksheets within the PFS will populate any field with a (schedule) listed. You only need to fill out the highlighted portions right now. This net worth calculator will controversially include your personal residence (homestead); however, I believe that for high-net-worth medical professionals, it is fair to include it. If you disagree, simply leave that section blank.

Assets

Cash on hand is how much money you keep in literal cash. Personal assets include watches, jewelry, art, antiques, furniture, and anything else you own of value. You should calculate these based on the price you could sell for them today, not the price you paid. Be realistic. This number is probably less than you think. The same goes for automobiles.

There is a section to fill out for gold and cryptocurrency. If you hold crypto in a publicly traded ETF, it will go in the securities section. You can also include partnership interests. Again, be realistic. How much could you actually sell your business for?

Liabilities

Include any credit card balance not paid off in full each month. You must manually enter any loans that are not mortgages, student loans, or personal notes payable. Include any taxes for which you are responsible but have not yet paid.

Net Worth

Once you have completely filled out the entire five-page PFS, you will have an accurate calculation of your net worth!

Part 3 – Personal Income/Expense Information

This is the section that really distinguishes the PFS from a traditional net worth statement. A bank wants to understand not only your assets and liabilities but also your income and the uses of your cash. A bank’s top priority is ensuring you are cashflow positive enough to remain solvent and repay your loan. Filling out this section with accurate numbers gives you a tight handle on your finances.

As you fill out this part of the PFS, only the middle column, “Last Year,” will be populated. As you complete the PFS year after year, you can just move the middle column to the left. The current year is the right column, which you must fill out with your projections.

Sources of Cash

Your gross salary should be entered along with any bonuses or commissions you receive; however, rental income will be automatically calculated as you fill out the PFS. Include any other business income and any sale of assets such as real estate. You can generally find all this information in your tax returns.

Uses of Cash

Calculate and enter how much you pay in both federal and state taxes. Most other categories will be automatically populated as you complete the PFS. If you have any other debt not accounted for, input it under “OTHER LOAN Payments.”

Net Cash Flow

The result of filling out part 3 is to learn your net cash flow, or how much of a cash cushion you have after accounting for all your expenses. Because your retirement and brokerage account investments (calculated in Schedule 9) are added to this form, your net cash flow is truly what you have left over after you have paid your bills and saved for the future. You can do whatever you want with what is left: invest it, spend it, save it, or give it away!

PAGE TWO

Schedule 1 – Cash in Financial Institutions

This one is simple. Just access your savings, checking, and money market accounts and input the balances.

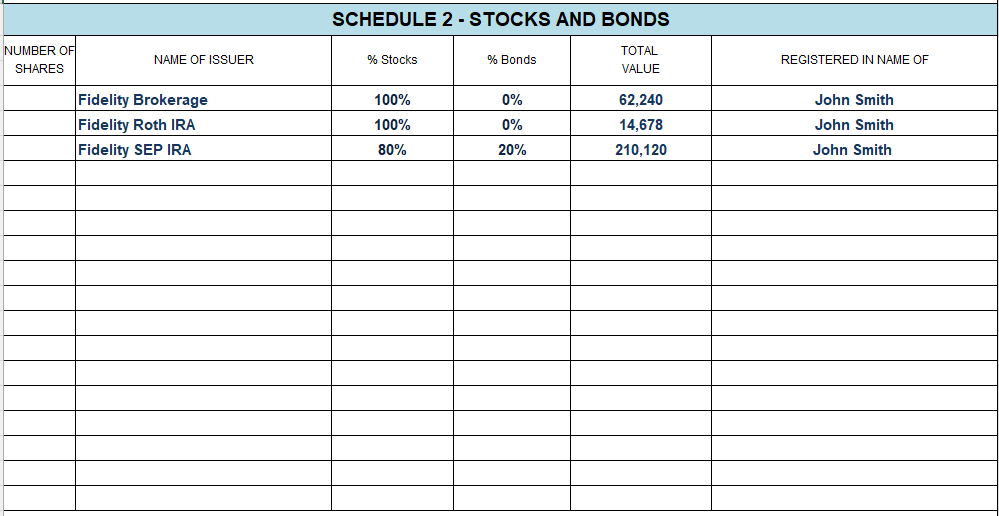

Schedule 2- Stocks and Bonds

This schedule is another easy one. Go to your retirement accounts and brokerage accounts and input the balances. I suggest you go into detail by entering your percentages of stocks and bonds in each account, which allows Schedule 10 to be calculated accurately.

Schedule 3/4 – Notes and Accounts Receivable/Payable

Schedule 3 asks for any private loans you have made. For example, Dr. Smith loaned a friend $50,000 to invest in a real estate project for one year at 15% interest. Include any private debt in Schedule 4.

PAGE THREE

Schedule 5 – Real Estate Owned

This section is my favorite, as real estate constitutes a large part of my assets. There are three sections in this schedule. The first is for investment real estate that you wholly own, which doesn’t mean you have to own the property free-and-clear; it just means that you have no partners and thus own 100% of the asset and cashflow and are responsible for 100% of any subsequent liability (mortgage).

The second section is for your homestead, or primary home. If you have a second home, include it in the first section and set the monthly income at zero unless you do short-term rentals.

The final section is for any partial interest in real estate, which includes real estate you own with partners, including syndications. Dr. Smith owns 50% of a rental property with a partner in this example. This PFS will automatically calculate your share of the assets and liability provided and transfer it to page 1.

This is another area in which you must be realistic with your market valuations. I have heard that banks automatically discount real estate valuations by at least 15% due to people inflating the market value. I personally wrote down a half million dollars on my portfolio this year because the Austin market has cooled considerably. How much is your real estate really worth right now after commissions? This is the time to be cold and calculating, not emotional.

Schedule 6 – Student Loans

Input your student loan balances and monthly payments into this section.

PAGE FOUR

Schedule 7 – Life Insurance

List any life insurance policies you have in this schedule. If you follow our advice on Business is the Best Medicine, you will only have a term life insurance policy, and your cash surrender value will be zero, like Dr. Smith. If you have a whole or variable life policy, the current surrender value will be included in your assets.

Schedule 8 – Monthly Budget

This schedule does not appear in a bank’s PFS. They only ask you to include your yearly expenses in the “Personal Income/Expense Information” on page 1. I added this schedule to incorporate a monthly budget into the PFS, making it more robust and allowing you to better understand where you spend your money.

You may want to change, add, or subtract headings in this schedule, as everyone has different categories of expenses. Note that if you rent, your rent payments go in your monthly budget, but if you own a home, your mortgage payments go under Schedule 5.

Schedule 9 – Automated Monthly Investing

I believe investing is as fundamental as anything else in your budget and that everyone should set up automatic investing. For this reason, our PFS considers retirement account contributions and brokerage account investments as recurring monthly expenses.

Many medical professionals have complicated financial lives. I max out my SEP IRA in a lump sum payment every January as it is easier than setting up recurring payments on the Vanguard website and gets the money invested sooner. While I automatically invest money into my brokerage account weekly, I also contribute occasional lump sums when I get distributions from my businesses.

If you make lump sum investments like me, you will have to calculate how much you invested into each account during the year, divide it into monthly contributions, and document it in this schedule. Don’t worry, the extra effort will pay off!

PAGE FIVE

Schedule 10 – Asset Allocation

Schedule 10 is a bonus I created for Business is the Best Medicine subscribers. As you fill out your PFS, your asset allocation will be automatically created! This allocation is based on your total assets and does not include contingent liabilities. Therefore, real estate may be overvalued if you are using leverage. However, it is still a good snapshot of where your assets lie.

My 2023 asset allocation was published here. I will update it soon, which will be easy using my latest PFS.

Conclusion

A personal financial statement provides a comprehensive overview of your finances. Banks want all your information in order to make an educated decision on your ability to repay a loan. They don’t just want your net worth but what constitutes it. They don’t just want your income but your net cash flow.

Use the same document as the banks do to track your financial life. This PFS can be modified to fit your particular financial circumstances. Do you own more than nine rental homes like I do? Add a few rows to the spreadsheet, or use the partial real estate owned section and just input 100%. Have additional income from a side hustle? Input it into the Personal Income Information section.

Use Business is the Best Medicine’s PFS to keep all your information up to date in an easy-to-use document. For the best results, fill out the PFS at the beginning of every year and track your net worth, net cash flow, and asset allocation over time!

I hope you benefit from this Personal Financial Statement as much as I have. You can download a FREE copy here or go to the resources tab at the top of the page. Thanks for reading, and please comment below with any questions or ideas.