I often feel like a black sheep when I hang out with people my own age. I have few interests in common with most people with whom I grew up, attended college, or went to PA school. It seems very few people think and talk about money and business endlessly like I do. So, why does financial independence matter so much to me? Hopefully, I can express my motivation in this article.

Start with STATS

The notes section on my phone is chaos – I’m constantly jotting down bits and pieces as I read, hear, or think of them. Sometimes, it’s something I want to research; other times, it’s an idea for an article. When I heard the following four items on a podcast recently, I immediately wrote them down – they encouraged me, reminding me that I’m taking the right steps to ensure I’m never part of these statistics.

Financial Reality:

1. The Income vs. Housing Gap:

In the last 15 years, salaries have risen by only 25%, while housing prices have climbed a massive 138%. If this trend continues, what will it mean for my kids when they try to buy their first homes? I’m determined to teach my children financial literacy so they don’t struggle with homeownership. I want them to be among the top 10% of people who truly know how to handle their money.

2. Cars vs. Freedom:

This statistic reflects a bigger challenge: the lure of high monthly payments on depreciating assets. My approach has been different. I bought my car back in college and paid it off within three years, giving me several years of freedom from car payments. Later, we bought a truck we couldn’t afford, but after 2 years of payments, we sold it for a more affordable, paid-off car, freeing up funds to launch our real estate business. Now, 10 years and 160,000 miles later, I’m still driving my paid-off car from college, and my husband rocks a minivan with our three kids in the back.

I cringe when I hear someone say they’re upgrading to a newer car for ‘just another hundred dollars a month.’ Those ‘small’ payments add up, trapping people in an endless cycle of debt. My kids might joke about my car’s ‘missing’ luxuries, like TVs and window shades, but I hope they’ll one day understand the real luxury of a paid-off car. Freedom from debt lets us focus on building wealth and choosing a life with fewer financial constraints. Financial literacy isn’t about impressing others today.

3. Debt Is Weighing Us Down:

The average person today carries about $70,000 in combined student and consumer debt. My first encounter with the concept of debt was in high school when I attended Dave Ramsey’s Financial Peace University at my church. While I don’t follow all his advice, his stance on debt struck a chord with me. Consumer debt isn’t a tool; it’s a burden. It’s why I prioritize paying off high-interest debt as quickly as possible and encourage others to do the same.

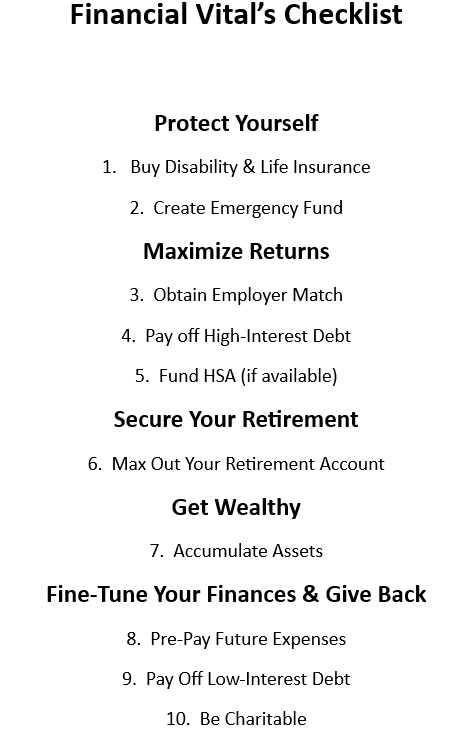

In Business is the Best Medicine’s Financial Vitals Checklist, a roadmap for building financial health, paying off high-interest debt is a crucial step—specifically, step 4. Mark Cuban once said, ‘If you use your credit cards, you do not want to be rich.’ He’s right—high-interest debt acts like an anchor, holding back financial progress. Paying off consumer debt is like getting a 25% return on your money every month by saving on interest. Eliminating this debt frees up cash flow, setting the foundation for building real wealth and moving closer to financial independence.

4. The Emergency Fund Crisis:

Nearly 60% of millennials have under $5,000 saved for emergencies, and 45% have under $1,000. These numbers make me cringe because I know this is my generation we’re talking about. We need to prioritize savings to secure our futures, and I’m determined to help my kids grow up understanding this.

Building a Legacy of Financial Literacy

Teaching my children about money is one of my core missions in life. It’s why I’m always working, thinking ahead, and learning more. My goal isn’t just to build a stable financial future for us—it’s to leave my kids a legacy of financial literacy. That’s why my five-year-old started his own little “business” this summer, and I couldn’t have been prouder. It’s a small start, but it shows him the value of earning, saving, and making smart choices with money.

Taking Responsibility: No One’s Coming to Save Me

Let me be clear: no one’s coming to save me. I didn’t grow up with trust funds or inheritances waiting to cushion my journey. My parents did a lot of things right when raising us, but demonstrating good financial habits wasn’t one of them. And that’s okay. I don’t dwell on what wasn’t handed to me; I take responsibility for my family’s future and am committed to changing our financial path. If I want a better life for my kids, it’s on me to make it happen.

America Needs Financial Independence, Too

This push for financial independence isn’t just for my family; I believe America needs it. We need more people to wake up to the state of their finances, recognize the trap of consumer debt, and reject the “buy now, pay later” lifestyle we’re constantly sold. Every day, we’re bombarded with the pressure to spend. But I want my children to see past that noise and know that they have the power to control their finances, not the other way around.

Standing Up to Corporate Medicine

Lately, corporate medicine groups (CMGs) and big healthcare corporations seem to be everywhere, taking over more and more of the medical field. And with that, we’re seeing less focus on actual patient care and more on profits. It’s exhausting, and I know it’s one of the reasons so many providers feel burnt out. But here’s the thing: our best way to fight back is by becoming financially independent. When you’re financially secure, you’re not forced to stay in a job that doesn’t align with your values or drains your energy just to pay the bills. Financial literacy gives us the freedom to choose workplaces that actually respect us and let us focus on what we went into medicine for in the first place—helping patients.

Building a Financial Legacy

My phone rarely shuts off because I’m juggling a lot: being a mom, running a business, staying engaged in my PA career, and sharing what I’ve learned with the next wave of medical professionals. I don’t want young PAs and APPs to hold off on investing or make the same mistakes I often see. I’m intentional about the lessons I pass on to my kids and those I might influence along the way.

Financial independence isn’t just a personal goal; it’s about creating a legacy that will guide my family for generations. My kids will grow up knowing about money, business, and what it takes to live free from financial stress. To me, that’s the real power of financial independence—it’s about leaving my kids equipped with the knowledge and freedom to make their own choices, to live without the burden of debt, and to pursue a life aligned with their values.

Conclusion

Financial independence means I can choose to live on my own terms. It allows me to walk away from environments that don’t align with my values, avoid the pressure to follow the latest financial “trends,” and give my family the stability to weather financial storms with an emergency fund. It’s not just about what I can accomplish today but about setting my children on a better path—one where they understand the value of hard work in business, making smart financial choices, and the real freedom that comes with financial independence.

This journey isn’t just about being debt-free; it’s about the freedom to make choices in our careers and our lives. It’s about building something lasting—a financial legacy prioritizing stability over status, purpose over possessions, and freedom over the endless cycle of consumer debt. And that’s a legacy I’m proud to build, not just for myself but for my family and anyone I might inspire along the way.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]